Definitions

- Supply: The total amount of a product or service available for purchase at various prices.

- Demand: The quantity of a product or service that consumers are willing to buy at different prices.

- Law of Supply: States that as the price of a good increases, the quantity supplied also increases, all else being equal.

- Law of Demand: Indicates that as the price of a good increases, the quantity demanded decreases, all else being equal.

- Market Equilibrium: The point where supply equals demand, and there is neither a surplus nor a shortage of goods.

- Surplus: Occurs when the quantity supplied exceeds the quantity demanded at a given price.

- Shortage: Happens when the quantity demanded exceeds the quantity supplied at a given price.

- Price Elasticity of Demand (PED): Measures how sensitive the quantity demanded is to a change in price.

- Price Elasticity of Supply (PES): Measures how sensitive the quantity supplied is to a change in price.

- Complementary Goods: Products that are often bought together, affecting each other’s demand.

- Substitute Goods: Products that can replace each other, affecting each other’s demand.

- Inferior Goods: Goods for which demand increases as income decreases.

- Normal Goods: Goods for which demand increases as income increases.

- Price Ceiling: A government-imposed limit on how high a price can be charged for a product.

- Price Floor: A government-imposed limit on how low a price can be charged for a product.

Diagrams

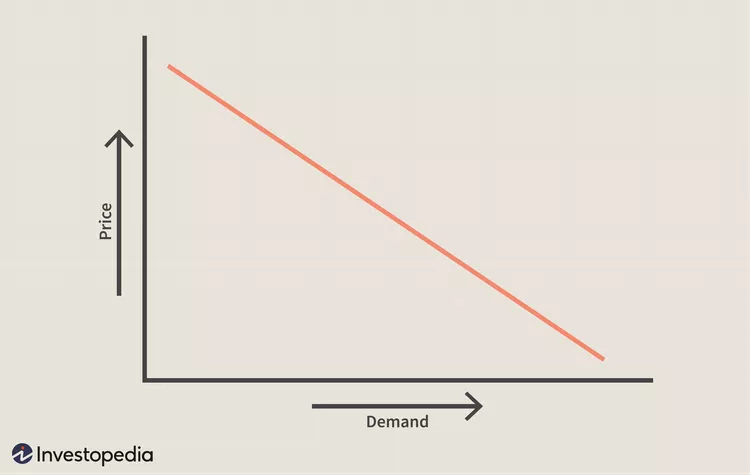

Figure 1: Demand Curve

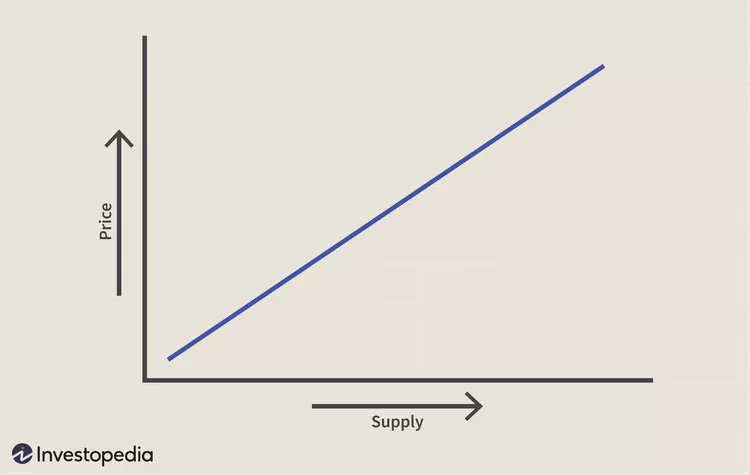

Figure 2: Supply Curve

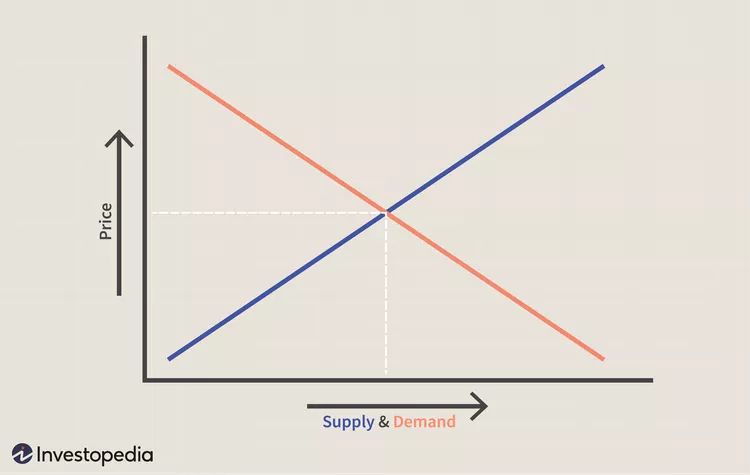

Figure 3: Supply and Demand

Supply

Supply refers to the total amount of a good or service that producers are willing and able to sell at different prices over a given time period.

The Law of Supply states that all else being equal, as the price of a good or service increases, the quantity supplied also increases. Conversely, as the price decreases, the quantity supplied decreases.

Factors affecting supply include:

- Cost of Production: Higher costs may reduce supply.

- Technology: Advances can increase supply.

- Government Policies: Taxes or subsidies can affect supply.

Price Elasticity of Supply measures how responsive the quantity supplied is to a change in price. Types include:

- Elastic Supply: A small change in price leads to a large change in quantity supplied.

- Inelastic Supply: A change in price results in a relatively smaller change in quantity supplied.

Types of Supply

- Individual Supply: Supply from a single producer.

- Market Supply: The total supply of a good in the market is the sum of all individual supplies.

Supply Curve

The supply curve graphically represents the relationship between the price of a good and the quantity supplied. It generally slopes upward, indicating the direct relationship between price and quantity supplied.

Want notes on other topics? You can check out our Edexcel A-Level Economics Notes here.

Demand

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various prices during a given period.

The Law of Demand states that, all else being equal, the quantity demanded increases as the price of a good or service decreases. Conversely, as the price increases, the quantity demanded decreases.

Several factors can influence demand:

- Income: As income rises, demand for normal goods usually increases.

- Tastes and Preferences: Changes in consumer tastes can significantly affect demand.

- Price of Related Goods: The demand for a good can be influenced by the price of its substitutes or complements.

This measures how sensitive the quantity demanded is to a change in price. It is categorized into:

- Elastic Demand: A small change in price leads to a large change in quantity demanded.

- Inelastic Demand: A change in price results in a relatively smaller change in quantity demanded.

Types of Demand

- Individual Demand: Demand for a good by an individual consumer.

- Market Demand: The total demand for a good in the market is the sum of all individual demands.

Demand Curve

The demand curve graphically represents the relationship between the price of a good and the quantity demanded. It generally slopes downward, indicating the inverse relationship between price and quantity demanded.

Want to test your knowledge? You can find A-Level Economics Past Paper Questions here.

Market Equilibrium

Market equilibrium occurs when the quantity demanded equals the quantity supplied at a specific price. At this point, there is neither a surplus nor a shortage of goods.

The price at which market equilibrium occurs is the equilibrium price. It balances the forces of supply and demand.

- Above Equilibrium Price: If the price is too high, supply exceeds demand, leading to a surplus.

- Below Equilibrium Price: If the price is too low, demand exceeds supply, causing a shortage.

Market forces naturally drive prices toward the equilibrium point. Surpluses cause prices to fall, while shortages cause them to rise.

Changes in supply or demand can shift the equilibrium price and quantity. For example, an increase in demand while supply remains constant will result in a higher equilibrium price.

Sometimes governments intervene to maintain price levels, using tools like price floors or ceilings.

Understanding market equilibrium helps in predicting market behavior and making informed decisions, both for consumers and producers.

Mark is an A-Level Economics tutor who has been teaching for 6 years. He holds a masters degree with distinction from the London School of Economics and an undergraduate degree from the University of Edinburgh.